Investing in real estate can be a huge wealth accelerant. Selenid and I have experienced this via our active real estate investments. They have been the biggest factor in the massive growth in our net worth. However, I totally get that most doctors are more interested in passive real estate investing.

But you still need to understand real estate investing to be successful passively. This includes understanding how sponsors are structuring the deal itself. Because, in the end, you are giving money to a sponsor and trusting them to invest it well.

And preferred equity is one of these ways. And it is becoming more prevalent.

For this reason, I've asked our partners at Crowdstreet to share the core information that physicians investing in passive real estate need to know!

Preferred equity 101 in passive real estate investing

In a commercial real estate market cycle, it can sometimes become challenging to acquire the appropriate amount and types of financing required to complete a purchase. One potential solution available to sponsors is the use of preferred equity. This helps fill in the missing puzzle pieces and move a project along.

What is preferred equity?

Preferred equity is a form of equity structured into a commercial real estate project as a way to create an investment. This, ideally, strikes a balance (both in risk and reward) between senior debt and common equity.

In this article, we’ll explain where preferred equity fits into a real estate transaction. We will also discuss its characteristics and highlight some of the pros and cons investors should consider when evaluating a preferred equity investment.

To understand preferred equity, it is important to understand its relation to other forms of capital that can be used to finance commercial real estate. This is the “capital stack”.

What is a capital stack and where does preferred equity sit within it in passive real estate investing?

A capital stack represents the structure of all the capital sources. It also represents their order of their repayment priority in a commercial real estate project.

Capital positioned higher in the stack generally has the highest risk of non-repayment. Because any potential distributions are paid last to the form of capital that has the highest position in the stack. As the perceived risk increases higher up in the capital stack, the potential returns may increase as well.

Most often, a capital stack often contains just two sources of capital, senior debt and common equity. However, it is possible to insert a middle layer of capital into a deal.

Preferred equity sits behind senior debt and ahead of common equity in a capital stack. You can get more in depth information about the capital stack via Crowdstreet resources here.

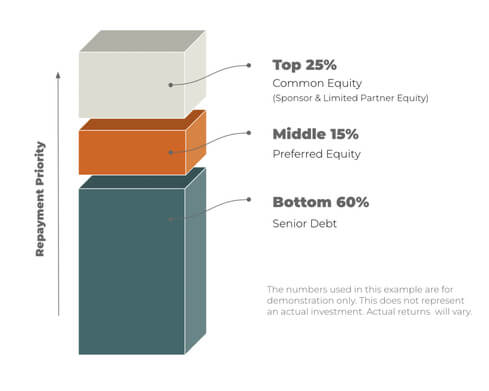

A case example

The capital stack depicted above is a three-layered stack with preferred equity coming in to fill the gap between a 60% Loan-to-Value (LTV) senior loan and a 25% common equity for the total project cost.

In this hypothetical situation, were the prevailing debt markets more competitive, a senior lender may well have provided a loan at 75% LTV instead of 60%. However, when a senior lender takes a more conservative stance and reduces debt proceeds, an operator or developer faces primarily two choices:

1. To increase the common equity, in this case, from 25% to 40% to fill the void. This can result in a dilution of targeted returns for those investors. This happens because profits are now being split between more equity dollars – although it is lower leverage so risk is reduced to some degree in this scenario.

2. To find a middle layer capital solution such as preferred equity to fill the gap. In this case, they need to fill between 60% and 75% in the capital stack.

What are the characteristics of preferred equity?

Preferred equity typically sits in the middle of the capital stack. Thus, this structure looks similar to debt or to common equity. The flexibility available to sponsors and investors to creatively structure preferred equity is part of the beauty of this form of investment.

Debt-like Preferred Equity

In its more certain form, preferred equity can possess features that simulate debt. So much so in fact that the IRS characterizes it as debt for tax purposes. Although not present in every deal structure, some similarities to debt may include,

- A pre-specified, fixed total rate of return – this is referred to as “non-participating” preferred equity because the investor does not participate in any additional potential upside

- A requirement for a certain level of return to be paid as it is due

- A maturity date that requires repayment (or “redemption”) regardless of whether or not the project is sold

- Extension options (typically with additional fees applied)

- An obligation to service the preferred return on a defined cadence (e.g. monthly or quarterly) – this is often referred to as “hard pay” preferred equity because there is an obligation to pay, regardless of the performance of the asset

- Fees, penalties and other consequences for failing to pay the current return as it is due

- A pre-funded preferred equity reserve from which payments can be made

- Reduced loss exposure in the capital stack (e.g. requiring that the subordinate common equity incur a 100% loss of invested capital prior to incurring any losses)

- Lower targeted returns in comparison to common equity positions

- Ability to protect the position of the investment in the event of a borrower default on the senior loan

Common-Equity like Preferred Equity

Although not present in every deal structure, similarities to common equity may include,

- No guarantee of payout. Distributions are based solely on the performance of the asset. This is often referred to as “soft pay” preferred equity. Because there is no obligation or guarantee to pay the preferred return if the project’s performance cannot support it

- Subordinate position to all debt in the capital stack in terms of repayment

- Profits participation – in essence, an uncapped upside. This is referred to as “participating” preferred equity because the investor participates in the potential upside depending on the performance of the asset

- Potentially higher targeted returns in comparison to debt positions and, even, to debt-like preferred equity positions

- Inability to protect the position of the investment in the event that a borrower defaults on the senior loan

How do investors get paid?

There are a number of ways to structure how payments or distributions are made in a preferred equity investment.

In many cases, the targeted rate of return is fixed and it is paid out to investors in two ways:

- Current return: An initial rate of return that is paid as it is due or paid “current” (e.g. monthly or quarterly payments). These payments may be made through the property’s cash flow or through a pre-funded preferred equity reserve during periods where sufficient cash flow to service the current return is not present.

- Accrued return: An additional rate of return that is earned as it is due but for which payments are deferred or “accrued” until a capital event, such as the sale or refinance of the asset.

A strong cash flowing project may predominantly use a current return structure. Conversely, a project low on cash flow, for instance a ground-up development, may need to rely on an accrued payment structure due to a lack of cash flow in roughly the first 18 to 24 months when the project is still under construction and stabilizing. In a current return scenario, investors are often willing to accept lower targeted returns because of the greater certainty of payments. In contrast, the more investors must rely upon accrued returns, the more risk premium (i.e. higher targeted returns) those investors will generally seek for taking on the uncertainty of waiting to be paid until the project stabilizes.

Investing in preferred equity: What’s in it for you as the investor?

Pros:

- Payment priority ahead of common equity

While preferred equity investors are typically offered lower returns compared to common equity investors, they are paid any potential returns first. This repayment priority may make an investment more attractive. This is especially so in uncertain times when the potential for high returns is also uncertain. Priority of repayment to preferred equity investors can be both for repayment of invested capital as well as for some to all of the preferred return. How much priority is given is usually negotiated when structuring the deal.

- Relative certainty of payment for stabilized assets

When an asset has a strong and durable net operating income, preferred equity can present a great way to receive regular distributions in exchange for potentially giving some upside away to common equity holders. Due to the fact that you typically receive your current return before any cash flow is distributed to common equity investors, you have more certainty of being potentially paid in comparison to common equity investors.

- Lower downside risk exposure than common equity

In the event that the asset does not perform as expected, which is always a risk, the common equity investors incur losses. And these losses can be potentially all the way up to 100% of their invested capital. This occurs before preferred equity investors incur their first dollar loss. In scenarios where you feel confident in an asset maintaining its value but you aren’t confident in a high level of profitability to the upside, a preferred equity investment may provide the optimal position for you in the capital stack.

Cons

- Lacks upside potential compared to common equity

In any investment, mitigating risk usually means giving up some upside reward in exchange. This is fundamentally true of preferred equity, too. If a project is successful, you should expect common equity investors to earn higher returns. Meanwhile you have the potential to either receive the targeted return you signed up for (in a non-participating preferred equity investment) or receive a bit of the upside but far less than what is paid to common equity investors (in a participating preferred equity investment)

- You can potentially lose 100% of your investment

While risk of loss is mitigated in a preferred equity position because of its repayment priority over common equity investors, it is still exposed to the risk of a full loss. In the event an asset with preferred equity is liquidated at a price that is below its position in the capital stack, the preferred equity investors would naturally incur a 100% loss along with the common equity investors. Therefore, preferred equity may be better suited for assets whose value is less binary. This includes multifamily investments where income streams can be diversified across often hundreds of tenants. Conversely, preferred equity may not be as well suited for single-tenant assets. This would be because losing the sole tenant could devastate its value and potentially wipe out all equity investors regardless of their status in repayment priority.

Uncertain times call for creative measures

The precipitous rise in interest rates throughout 2022 and 2023 has significantly reduced the amount of debt available to finance commercial real estate deals.

One solution increasingly sought in recent months is the use of preferred equity. It allows for compensation of the gaps left by more conservative debt financing.

Structuring a preferred equity component into a capital stack can add momentum and move projects along as it fills in the missing piece.

Ultimately, preferred equity can provide a creative form of financing. If used strategically to strike the appropriate balance of risk and reward, can result in a win-win scenario for both the investor and the sponsor.

My take (Jordan here again) is that preferred equity in passive real estate investing in neither bad nor good necessarily. But it is something that every investor needs to understand. Because it does impact returns. And can be used well or used poorly.

The more you know, the better set up you are as an investor!

Interested in learning more about passive real estate investing?

- Visit Crowdstreet to learn more or see their available deals!

- Check out these other posts!

What do you think? Is preferred equity good or bad? Have you come across passive real estate investing deals with preferred equity? Let me know in the comments below!

*Disclaimers here!