In his famous book, Rich Dad, Poor Dad, Robert Kiyosaki introduces the concept of the cash flow statement. (He technically calls it an income statement but I like cash flow statement better.) It's basically a simple diagram to help show in general terms where your money is coming from and where it goes. Like all good learning supplements, its impact despite its simplicity is tremendous.

The idea and concept of the cash flow statement was one thing that really got me to understand why my financial well-being was so poor. It also helped me understand how doctors, despite being very high income individuals, can be living pay check to pay check.

But most importantly, it gave me a blueprint for achieving financial freedom.

So let's dig into my cash flow statement to hopefully demonstrate why it is such an impactful concept and how you can create your own and get it working for you!

The basics of a cash flow statement

Like I said, it's very simple.

The top two boxes represent your income and your expenses

Your income is any money coming in that you earn, actively or passively. Examples include W2 or 1099 doctor income, passive cash flow from dividend stocks or real estate, income from side gigs and so on.

Your expenses box is filled with anything that immediately takes money out of your pocket on a regular monthly basis. This would be things like groceries, entertainment expenses, and the like.

The bottom two boxes represent your assets and liabilities

On the left is your assets. These are things that you buy that put money into your pocket. Things like stocks, bonds, cash flowing real estate, passive side gigs, etc.

And then on the right is your liabilities. These are things that you buy that take money out of your pocket – that become monthly expenses. This box is filled with things like car leases or loans, mortgages on non-cash flowing property, debt, etc.

And these four boxes interact together

You can already start to imagine some of these interactions.

We have three choices with our income. We can:

- Buy assets that create more income,

- Buy liabilities that create expenses, or

- Spend it on immediate expenses

Often, we do some combination of all three with our income. But the proportion we allocate to each box will determine if we own our finances or if they own us. They determine our financial freedom.

Because remember, it's not how much money you make, it's what you do with that money that's important! That's how you build net worth.

Analyzing my cash flow statement

I'm going to build my cash flow statement as I was when I started learning about this stuff 3ish years ago. As we go along, it will re-create my current statement. But this will allow us to all see how I went from poor financial well-being to the road to financial freedom.

Step 1: My income

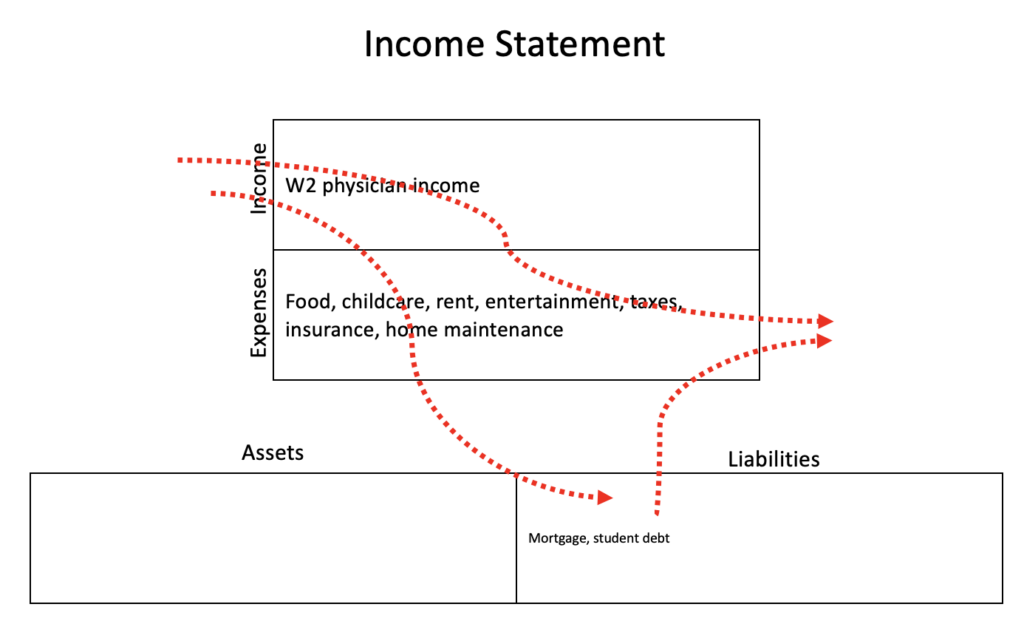

This started out pretty simple. My income was my W2 income as a doctor. For simplicity, I am keeping out Selenid's income. But that would go here as well.

Step 2: Expenses

Also pretty simple at this point.

Basically, my expenses were everything that I spent money on. Our rent when we started tracking this in NYC, food, eating out, entertainment, loans, insurance, taxes, and things like that.

Our biggest expenses were and remain our home and childcare as you can see in my money flow map here.

Step 3: Liabilities

Now, let's add in my liabilities…

Our biggest liability was always my student loans. Plus we had credit card debt to start out. Add in a new mortgage and a car lease for Selenid's car (not mine!), and we were rolling in liabilities…

And you can start to see where the problem is…

Especially when we look at the flow of money with a cash flow statement like this.

My income statement looked like a water bucket with a big hole in the bottom. My money came in via income and then I spent it on expenses. Or I spent it on liabilities which then became expenses.

In on one side and right out on the other.

This is the stereotypical income statement of someone with low financial well-being and net worth.

Something had to change…and thankfully, with some education and effort, it did!

Now, step 4 and step 5 kind of happened concurrently but I'm going to separate them here.

Step 4: Reducing liabilities

This was the first change that Selenid and I made. And it's not surprising because getting out of debt was our #1 financial goal and thus paying off liabilities became a top financial priority in our written financial plan.

So, over 3 years, we paid off all of our credit card debt, bought Selenid's car in cash to eliminate the lease, and paid off 65% of my private student loans.

Now, our cash flow statement looks like this:

This was better. But still there was an issue. We lacked assets. And without assets, we kept needed to work to cover our expenses. We were still living pay check to pay check.

Step 5: Building assets

We needed to start buying assets that would put money back into our pockets. So we did.

And the way we started to do this was to invest in index funds of stocks and bonds along with real estate investment trusts (REITs) based on our asset allocation as set out in our written personal financial plan. (Here is a great guide to help choose your own asset allocation.)

And we then invested these in accounts based on our investment waterfall.

These investments create capital gains that may not add directly to our cash flow now, but will in the future. Some may argue that this doesn't count for the cash flow statement. But I think that's splitting hairs. I count it.

Then, Selenid and I started to buy cash flowing rental properties based on our deal criteria laid out here. These properties create cash flow that covers their mortgage and all expenses with extra going into our pocket every month.

It started with 1 duplex creating $1,000 monthly of cash flow and now totals 8 properties with $11k+ monthly in cash flow.

Step 6: Creating additional income streams

There are tons of ways to do this.

I did it via:

- Real estate investing as above

- Through my blog

- Medical consulting and surveys (here are the medical survey companies that I use)

Not all are passive but may are more passive than my W2 doctor income.

You can learn more about finding physician side gigs here or medical consulting opportunities here.

The bottom line is this super charged my income to allow for buying more assets which created more passive income.

Step 7: Fine tuning my cash flow statement

For us at this point, most of our expenses were stable, well controlled, and aligned with intentional spending.

However, one expenses remained very high. And that was taxes. So, we started to implement tax strategies to legally minimize our tax burden. These included:

- Investing in tax deferred investment accounts,

- Using my side gigs with 1099 income to write off expenses, and

- Using real estate to create passive losses to offset active gains with REPS

You can find more tax strategies for physicians here.

This ultimately reduced our tax burden and led to our current cash flow statement which looks like this:

Now, this income statement is one that will lead us to financial freedom!

A few important last notes

1. You'll see that my cash flow statement is not all green lines. We still have expenses and liabilities.

Now, we aggressively are attacking our liabilities by paying off extra to our mortgage each month and paying down student loans. And we control our expenses using a budget and the concepts of intentional spending.

But, the reality is that we will always have expenses. The cash flow statement is not about getting all green. But it's about establishing the right balance so that you are creating renewable, non-active income and investments so that you can reach a point of financial freedom.

2. My cash flow statement has a lot of lines. It took me awhile to sort through everything that first time I read about these concepts.

If it's not clicking right away, take some time to sit with it. Follow each line one at a time.

Make sure you understand the concepts.

3. Sit with a piece of scrap paper and draw out your own cash flow statement. See if it aligns with what you want it to look like.

Is it helping or hurting you? And what can you do to improve it? It's a powerful exercise. One that helped set the stage for Selenid and I to grow our net worth by almost $1 million in a few years!

And if you are looking for a complete guide to financial freedom for physicians with concise, actionable steps, check out my best-selling book, Money Matters in Medicine!

What do you think? What does your cash flow statement look like? How have you adjusted it? Let me know in the comments below!

One Response

Great piece and thanks for showing us how your cash flow statement has changed over the years. Examples almost always help the lesson stick.