Real estate feels different right now. And I don’t mean that in a vague or emotional way. I mean it in a measurable way.

- Lightstone Group is a $12B real estate platform with nearly 40 years of experience. Through Lightstone Direct, investors access the same deals they invest in themselves, with Lightstone typically co-investing ~20% of the equity.

-

If you're exploring passive real estate income outside of medicine, you can submit a short form to see whether their current opportunities may be a fit.

Request an intro here - Want to understand the market reset first? Join our webinar where we break down why real estate prices fell 20–35%, why supply may drop 65%, and why 2026 could mark the start of the next cycle.

From 2022 through 2024:

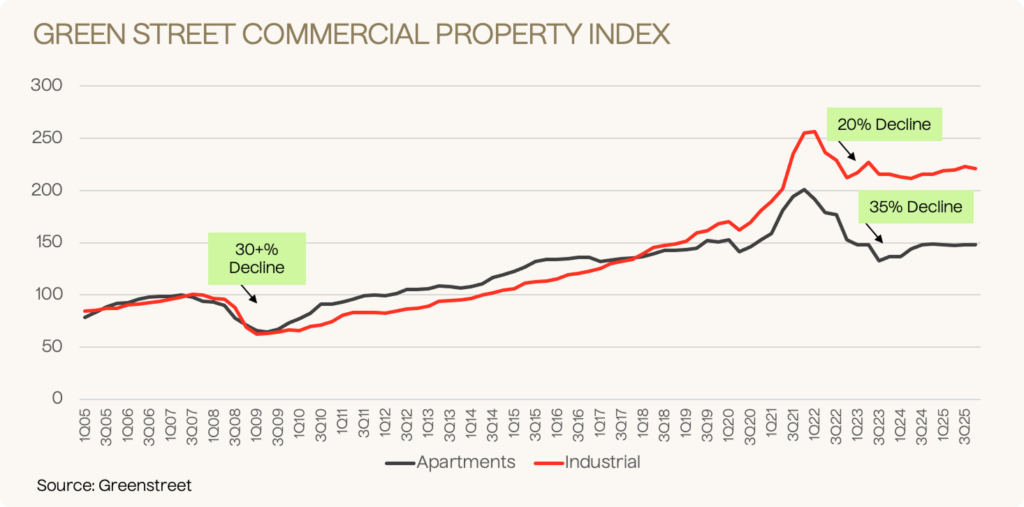

- Multifamily property values declined roughly 35%

- Industrial property values fell about 20%

- Transaction volume dropped sharply

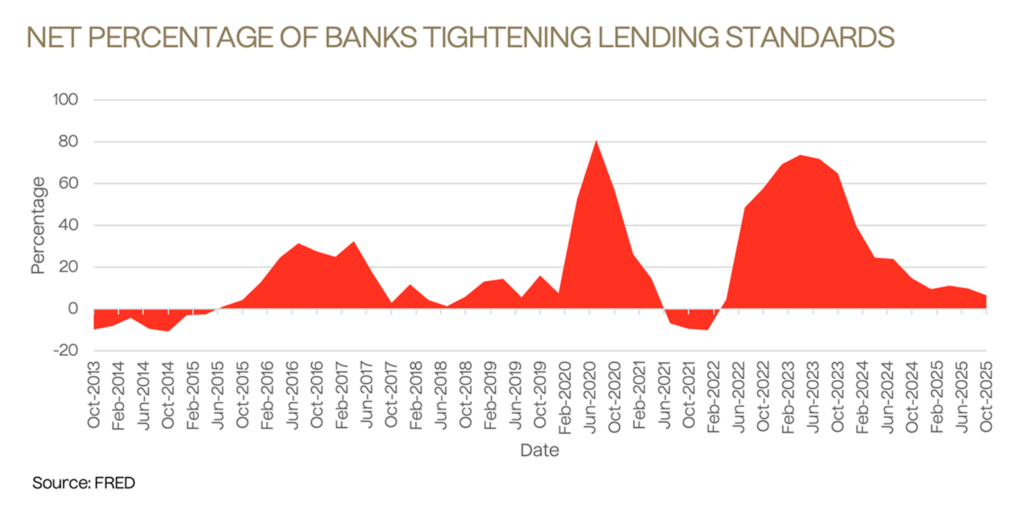

- Regional banks pulled back from lending

- A wave of new apartment supply hit the market

That’s not a small correction. It’s a 20–35% repricing across two of the largest real estate sectors. And in investing, repricing cycles often create the most interesting opportunities.

In other words, real estate didn’t quietly slow down. It went through a full repricing cycle, and that reset sets the stage for everything happening in the market today.

Cheap Money Made Everyone Look Smart

For most of the 2010s, real estate felt almost automatic.

Interest rates were low. Borrowing was cheap. Property values kept rising. Rents kept going up. You could buy a decent property, hold it, and the market would often bail you out.

It wasn’t that skill didn’t matter.

But it mattered less.

Then interest rates rose faster than they had in forty years.

Suddenly:

- Mortgage and loan costs doubled

- New construction projects stalled

- Property values corrected

- Investors could no longer rely on “easy appreciation”

According to the Green Street Commercial Property Pricing Index, from peak to trough:

- Apartment (multifamily) values fell about 35%

- Industrial properties fell about 20%

That’s a reset. That shift from cheap money to expensive capital is what forced the market to reset and pushed investors back toward fundamentals.

A Few Quick Definitions

A few quick definitions if you don’t follow real estate closely. Multifamily refers to apartment buildings with five or more units. Industrial properties are warehouses and logistics facilities. Class A buildings are newer luxury properties, while Class B properties are older but well maintained workforce housing.

You will also hear the word “deliveries,” which simply means newly completed buildings that hit the rental market. When a large number of new properties are delivered at the same time, rents often flatten temporarily as supply catches up with demand.

Understanding how supply and demand move through these property types helps explain why the market corrected so sharply over the last two years.

Here’s What Didn’t Break

The surprising part of the last two years is that property income held up better than expected.

Across Lightstone’s $12B portfolio:

- 21 industrial leases were signed in 2025

- More than 1.1 million square feet leased

- 19 of the 21 leases were signed above projected rent

With no rent concessions.

On the apartment side:

- Rents grew 3.0% year over year

- Net operating income grew 4.7%

Performance exceeded internal targets. This is real operating data we can leverage as an example. So while real estate prices reset, the underlying income from many properties proved far more durable than many investors expected.

The Supply Surge Is Already Fading

One of the biggest headwinds over the last two years was new construction.

Developers who locked in cheap loans during COVID built aggressively. Those projects were completed in 2023 and 2024.That surge of new “deliveries” hit the luxury apartment market especially hard.

When a lot of new buildings open at once:

- Landlords offer free months of rent (called concessions)

- Effective rents flatten

- Some markets see temporary rent declines

But here’s what’s happening now:

New construction starts have dropped dramatically.Because borrowing costs are higher and lenders are cautious, projected annual apartment deliveries are expected to decline by more than 65% by 2027.That’s not a mild slowdown, that is more like a major drop in future supply.

Meanwhile:

- Household formation continues

- Homeownership remains unaffordable for many

- Demand for workforce housing remains strong

When fewer new units are being built but people still need housing, the long-term setup improves. If supply continues shrinking while demand remains steady, the balance of the market could begin shifting back toward property owners.

- Lightstone Group is a $12B real estate platform with nearly 40 years of experience. Through Lightstone Direct, investors access the same deals they invest in themselves, with Lightstone typically co-investing ~20% of the equity.

-

If you're exploring passive real estate income outside of medicine, you can submit a short form to see whether their current opportunities may be a fit.

Request an intro here - Want to understand the market reset first? Join our webinar where we break down why real estate prices fell 20–35%, why supply may drop 65%, and why 2026 could mark the start of the next cycle.

Liquidity Is Quietly Returning

From 2022 to 2024, many banks pulled back from commercial real estate lending.Transactions slowed. Buyers and sellers couldn’t agree on pricing. Everyone waited.

Now we’re seeing:

- Apartment and industrial transaction volume rebounding from 2023 lows

- Buyers and sellers increasingly aligned on pricing

- Lenders slowly re-engaging

This doesn’t mean we’re back to the frenzy of 2021 but the reset is where a disciplined investor can start making deals. As pricing stabilizes and lenders return, the market is slowly moving from a period of uncertainty toward a period where deals can start happening again.

Not All Real Estate Is Created Equal

During the easy-money era, luxury properties in big “headline” cities attracted enormous capital but in reality all that matters is cash flow and there are investment areas where cash flow is king.

Specifically:

- Class B and A-minus apartments (solid, middle-market housing)

- Well-located industrial buildings

- Middle-market cities

- Properties that generate strong income from day one

Why? Because if a property works based on today’s income, you don’t need heroic assumptions about future rent growth or perfect timing on sale. And in a higher-rate environment, properties that produce reliable income today tend to become far more attractive than properties that rely on future appreciation.

A Simple Reality Check

In real estate, you typically get one of two things:

- Higher current cash flow

- Higher projected upside at sale

You rarely get both without stretching assumptions.If someone is promising high income today and massive returns tomorrow, it’s worth asking: Where is that return really coming from?

In the last real estate boom of easy money, many deals depended heavily on rising property values to make the math work. In 2026 and beyond, income matters more. That shift back toward income is one of the biggest ways the current real estate cycle differs from the previous one.

Why “Boring” Can Be Safer

The markets that didn’t boom as aggressively often didn’t crash as hard.Some Sun Belt cities saw huge capital inflows and aggressive building during the boom years. When interest rates rose and supply peaked, those same markets experienced flat or negative rent growth and heavy concessions.

Meanwhile, many middle-market cities where workforce housing dominates didn’t end up experiencing the same run up…so they didn’t require the painful correction. In other words, the markets that avoided the biggest boom often avoided the biggest correction as well.

Why 2026 Feels Like a Turning Point

Look at the sequence:

2022–2024

Property values fell

Liquidity dried up

New supply peaked

2025

Pricing stabilized

Transaction volumes rebounded

New development slowed sharply

2026 and beyond

Supply pipeline contracts

Capital re-engages

Income remains intact

After a 20–35% repricing and a 65% projected drop in future apartment deliveries, the risk/reward dynamic looks very different than it did three years ago. When pricing resets, supply slows, and capital begins returning at the same time, it often signals the start of a new phase in the real estate cycle.

Putting It Into Practice

One reason I’ve partnered with Lightstone for educational discussions is because their approach reflects this shift. Over nearly forty years and $12B invested, they’ve:

- Focused on durable cash flow

- Avoided chasing trends

- Invested their own capital alongside partners

- Operated through multiple cycles

Through Lightstone Direct, individual investors can access the same types of properties they invest in themselves. That alignment matters. And in a market that has just gone through a major reset, experience and disciplined underwriting matter more than ever.

- Lightstone Group is a $12B real estate platform with nearly 40 years of experience. Through Lightstone Direct, investors access the same deals they invest in themselves, with Lightstone typically co-investing ~20% of the equity.

-

If you're exploring passive real estate income outside of medicine, you can submit a short form to see whether their current opportunities may be a fit.

Request an intro here - Want to understand the market reset first? Join our webinar where we break down why real estate prices fell 20–35%, why supply may drop 65%, and why 2026 could mark the start of the next cycle.

One Response

Many markets are experiencing a subtle adjustment rather than dramatic shifts. These quieter resets often create more balanced conditions.