It seems counterintuitive. Here I am writing this, 1.2 years out of my training and I'm talking about retirement. But this should not be the exception, it should be the norm. And I didn't start out this way… but the best time to think about retirement is before doctors even start working. Plan ahead and you can control your time, work because you want to, not because you have to, and retire comfortably on your terms. To help you do this, I've developed a simple 5 step retirement calculator for doctors that I'd like to share with you all.

Let's walk through the retirement calculator for doctors together

Step by step…

Oh yeah…if you want to download this calculator for free, just use the side bar over on the right side here –>

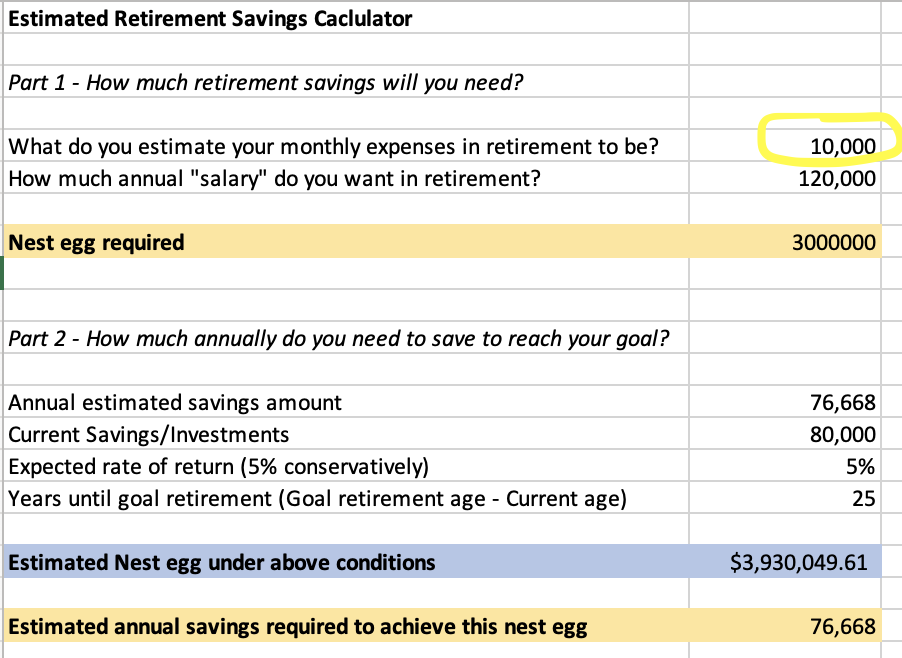

Step 1: Figure out how much monthly expenses you want/need to cover in retirement

Once you enter retirement, you exit the accumulation phase of your financial life cycle.

So, in the purest sense, you are no longer worried about your active income covering your monthly expenses.

You now are going to use your savings and investments to cover all expenses. That's how you retire and live each day however you want.

Doesn't mean you can't still make money. Plenty of “retired” folk do. But we are keeping it pure. Plus it's always better to know you can retire without income and then have any income be the cherry on top.

Anyway I digress…

The first step in the retirement calculator for doctors is figuring out your monthly expenses.

To do this, sit with your budget (use my template here). Go through your expenses and think about how these will change in retirement.

For example you will need to make sure you include:

- Healthcare if not Medicare age

- School expenses if kids are not yet through their education (Here are some tips)

- Long term care costs

- Vacations

Some examples of things you will no longer need include:

- Life insurance

- Disability insurance

- Student loans

- Consumer debt

- Hopefully your mortgage since you will have paid this off

I recommend always overestimating how much you want/need.

Step 2: Calculate yearly expenses

This step is a gimme…multiply your number from Step 1 by 12.

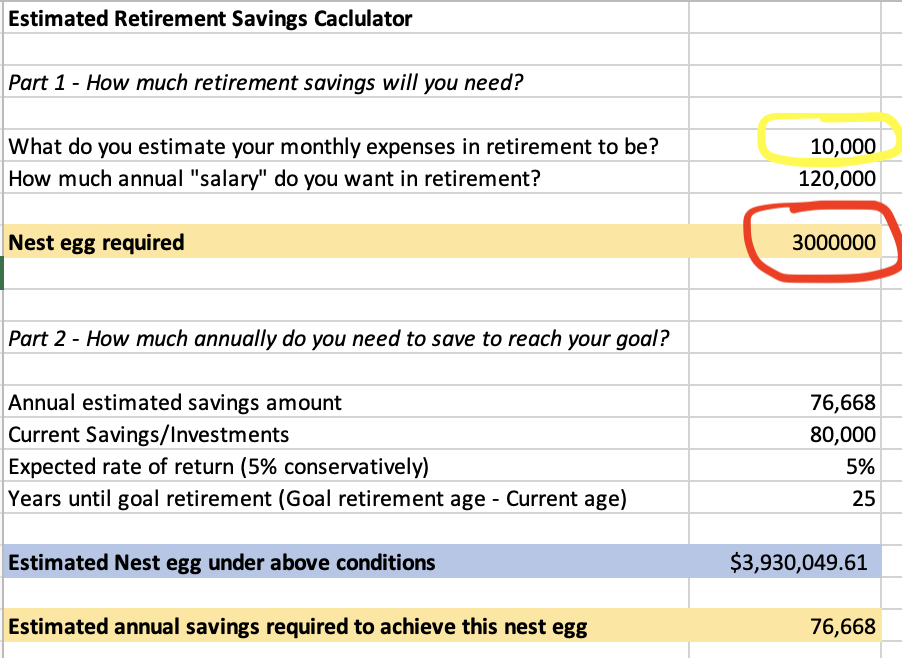

Step 3: Determine how much nest egg you will need

Once you know how much money you want/need to have in retirement on a yearly basis, you can figure out the nest egg you will need to achieve that.

It's a simple equation based on the 4% rule.

Remember, the 4% rule is based on the Trinity study which showed that you can safely withdraw 4% of your investment nest egg each year in retirement and have a very high chance of not running out of savings before you die.

Before people get up in arms, this is a ground rule…a rule of thumb…a guideline. It is by no means perfect. But it's a great way to make these estimates.

For more detailed information on the 4% rule, check out this post.

Anyway, if you divide your yearly desired retirement expenses by 4% (or multiply by 25), you get the nest egg required to sustain your retirement.

But don't stop there…you still need to figure out how to put that nest egg together

And that is what the second half of the retirement calculator for doctors is designed to help you with

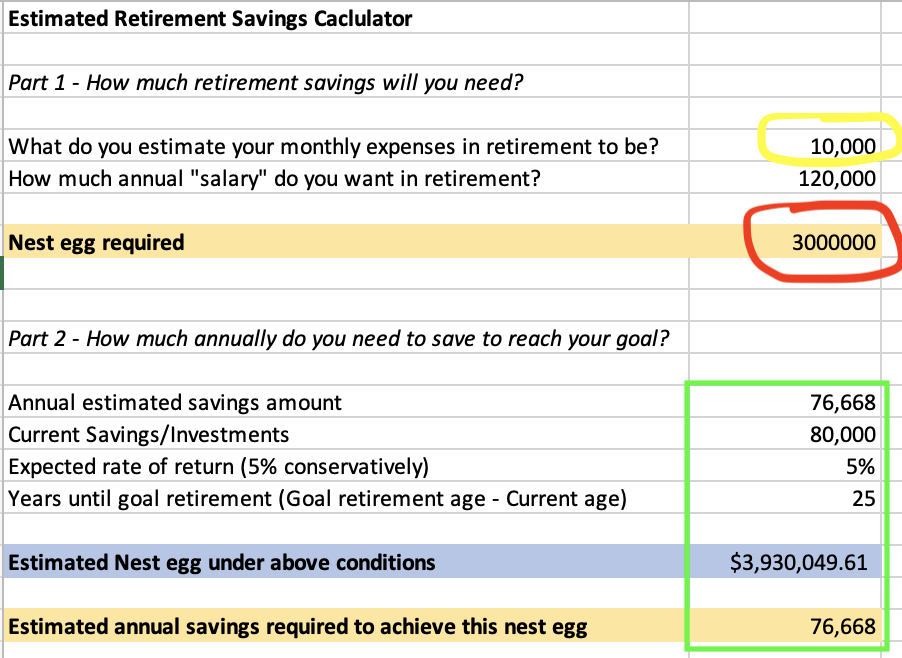

Step 4: Determine your required savings rate

Remember, the key to achieving financial freedom is simple.

Increase the difference between what you make and what you spend. This is your “margin.”

Then invest this margin.

So, to reach your retirement nest egg you need to figure out 4 main variables.

- How much you need to save each year

- How much you already have saved

- Your expected rate of return on your savings

- How long you have until you plan to retire

These 4 variables will largely determine the nest egg that you retire with

And the cool thing is that they are relatively in your control. #1, #2, and #4 are definitely in your control.

And with a thought out written financial plan in your pocket, #3 becomes more and more controllable.

So, in Part 2 of the retirement calculator for doctors, first enter your current savings and how long you plan to work until you retire.

Next, enter your expected after tax, after fees return on your investments. Be conservative. Better to underestimate and have more later on than vice versa.

Then, play around with your annual savings

As you do this, you will see that your expected nest eggs will change.

That way, you can play around with these variables until you see that you meet your desired nest egg.

Now you have all of the information needed to start building towards that nest egg!

N.B. This calculator does not directly factor in forms of passive income that can sustain you during retirement

Things like rental income or dividends. What Selenid and I do is subtract that expected yearly total of passive income from our expected yearly expenses. Then we calculate the savings needed to reach a now amended nest egg based on the amended yearly savings.

For example, let's say we expect to have yearly expenses of $200,000. But we have rental income of $100,000/year. Then, we would really only need to cover $100,000 ($200,000-$100,000) in annual expenses. This equals a nest egg of roughly $2.5M compared to compared to $5.1M without the rental income.

I hope this also demonstrates just how powerful passive income can be! You can learn about how Selenid and I generated $60K in passive income in just one year here!

Step 5: Enact your plan!

This is the most important step.

I have seen and know so many people who will spend hours and hours running these calculations. But then they don't change their spending habits or increase their savings or invest their money (wisely or at all)!

What you have effectively done in steps #1-4 is create a plan to reach your goal retirement on your terms.

It's in your hands now.

It's within reach!

Now all you need to do is to create those savings, invest that money wisely, and follow your plan to reach financial freedom!

And as a bonus, check out these physician side gigs to make you passive money!

You can also save the hours and hours of reading that I did to figure all this out and check out my course, Graduating to Success, where I condense all of this into high yield information that I promise will deliver you financial freedom. I think that is well worth the cost!

You can learn more about my course here.

What do you think? Have you calculated your desired nest egg? What about your plan to reach that nest egg? Let me know in the comments below!

Check out my free masterclass webinar, 12 Steps to Financial Freedom for Physicians here!

16 Responses

I think it would be extremely difficult for most doctors to save 75k a year after paying mortgage, taxes, insurance and family/ kids expenses, as most doctors earn between 200k to 3500k. After taxes, they get 120k to 210k.

The numbers here are an example. As a rule of thumb, everyone should strive to save at least 20% of their gross income and invest it wisely in broadly diversified index funds. On a $200k salary, this is $40k. On a $500k salary, this is $100k.

I respectfully argue that if you can’t save 20% of your gross income as a doctor, you have a spending and saving problem, not an income problem.

Agreed. See “The Millionaire Next Door,” among others. Thank heavens my Dad was cheap as hell, and taught me about investing early. Doesn’t eliminate mistakes, but puts you one leg up.

I’ll be honest, haven’t read enough of your stuff to know your take on tax-risk diversification as well as the issues of using disparate income sources and withdrawal sequences (guaranteed, RMD, pre/post tax brokerage, whole life, etc). There’s abundant literature on that as well, of course. Be mindful of the author’s motivations….

Im a big fan of tax risk diversification with tax deferred, tax free and taxable accounts being diversified and leveraged with most tax inefficient vehicles like REITs/bonds in tax advantaged accounts. Also a big fan of multiple streams of income which is why I am so big into real estate!

you need to work at Kaiser Permanente. they put in $80-90K/year for free into my pension. then there is another 18K into 401K. you could put max about $50K if you are able. essentially 40% of salary as the pension for 20 years of service and 50% if 30 years of service. benefits can start as early as 55 (with reduced benefits) or full benefits at 60 years.

But none of that matters if you can invest well. I cannot see how I can even start to touch that pension given my investments in last 10 years. Granted I made my first millions in real estate then in stocks.

Max out 401k

20k or 30k if over 50

(Match not included)

Max out 457

~20k

Max out Roth IRA (backdoor)

7k or 14k (spouse)

HSA

~8k

20k + 14k + 8k =42 K (skipping 457)

(Match minimum 10-15k)

Already in 50k range

This is bare minimum at income around 250k should be able to do this; if can’t then your lifetime expectations are out of alignment

The one thing you left out is taxes. Retirement income that doesn’t come from savings is taxed. Social security is taxed if you earn more than 15 or 20 thousand dollars. I cannot figure out how much I will have to pay in taxes and that throws off all the other calculations. So, if retirement involves money in a 401k or 403b or any passive or active income, then how do you figure out what you’ll be left with after taxes? We can’t all survive on just our savings account or post-tax money.

You’re right, this is the great unknown and always subject to change. How do I account for this? I overestimate my expenses by about 30%. That 30% is taxes…

I think a lot of this is incredibly over-simplified. Think about your parents and your spouses parents — do they have their lives well planned out? Then you have your own children. We have one adult child who has an incredibly risky job and could become disabled for life drastically changing our personal commitments and his spouses’ circumstances too. What about our future grandchildren? Who will fund their education and opportunities? We also feel obligated to contribute to society and academic institutions. We planted 1,500 trees over the summer to help mitigate our personal carbon footprint. We fully intend to leave this world much better than we arrived in it. It is a moral imperative to give back, contribute and exhibit leadership by personal example.

That’s great! Include all of this when estimating your expenses for retirement

No, you are CHOOSING to make it more complex. It’s still numbers. Estimate them. With a margin.

great points all of the above.

None of anyone’s calculations work if you get divorced…especially in a community property State such as California. Wealth can not be divided to achieve these goals….So…either 1) never get married

2) marry someone who asks YOU to sign a prenuptial agreement (ie they have more money than you)

3) get married for the first time AFTER you retire

I agree with Mr. Taylor above. The concept of multiply x 25 your annual expenses does simplify the calculation of what you need in retirement and is helpful as a guideline. Those of us who have our savings in retirement accounts need to know that when you take that money out of your savings, it will be taxed. There will be federal, state, and FICA (medicare and social security), and property taxes – some of this dependent on which state you live. I am not including Roth’s or “passive” income. I am not sure if someone has a way to figure this out more accurately, but I divide the amount I need monthly/yearly in retirement by 0.61 (39% total taxes?) and this gives me a general dollar amount as to my needs. Then I will find a tax calculator, asking your browser, “How much is left after taxes of (your number; i.e. $200,000) in (your state)” and several calculators will come up that you will give you a result that is more accurate for planning purposes in the future. Yes, the number is more realistic (and for some like myself-depressing), but I think you will have better information. My possible solution is to continue working in “retirement,” though at my pace (and a different clinical environment) with the assumption that my mind and body allow me the ability to work as long as I am able.

I think you are right in including taxes as part of your expected expenses on retirement. The rate is an estimate but this is important to include!

Your marginal rate wouldn’t be 40%. Closer to 30% depending on the amount you are spending. If you’re lucky/skilled enough to budget over $400k a year in retirement, well, you have a good problem. For instance, the tax rate on income over 170k (couples) is 24%. Substantially less on the income below that. Doesn’t reach 32% until about 340k.

Bear in mind that most of the (insert adjective) tax penalties that are imposed on high earners (not talkin’ about just the rate here) disappear in retirement if your planned withdrawals are less than 250k. This includes the absurd 3.8% surcharge on investment income for earners over 250k.

This is all subject to change. Congress will undoubtedly try to find ways to take more of our money to finance their profligate spending. The interest on the national debt alone is set to skyrocket shortly even without any changes to the rest of the budget. So perhaps your technique is the simplest and best (count on 40% taxes).

The solution to the state tax issue….move to a state with no or very low taxes. Keep in mind estate taxes/laws as well.

One thing not mentioned is the fact that your Medicare premiums are determined by your income the year before you sign up (year you turn 64). So it may be wise to plan for lower income that year if at all possible. The premium by income scale is easily searchable.

There are a lot of moving parts. Unless you’re a tax atty or accountant, or CFP, or just really enjoy Rube Goldberg, I think PPS has the right idea. KISS. Just use a margin for…governmental bad behaviour.

The 4% rule is much too simple.

The end result is zero at 30 years. That’s not a risk I wish to take.

Whether your retirement funds are tax deferred (Ira, 401k etc) vs regular brokerage accounts is very important and rarely discussed.

Tax deferred accounts are taxed as ordinary income and in regular accounts only the capital gains are taxed.

This could be the difference between a marginal tax rate of 30+% vs less than 20 percent. There are some sophisticated software programs that can help sort this out.

At the end of the day, you need calculate expected AFTER TAX expected expenses.

Depending on where you savings are located, how much savings you have, could potentially affect after tax spend by 40-50%