Well, it's officially 2026. And that means our investing performance for 2025 is locked in! As I usually do, a few weeks ago I was going over my investment accounts and thought it would be fun to share how Selenid and I did. So, here is our 2025 portfolio performance.

But first…

• Locumstory is the simplest explainer I’ve seen for locums. What it is, how it started, and what it looks like in your specialty.

• Take the “Are you ready for locums?” quiz, compare agencies, and run through their free crash course.

• If you want the truth, not the hype: pay ranges, taxes, multi-state headaches, and real physician stories.

The rules of the game

This is how this 2025 portfolio performance review is going to work:

- I’m going to go account by account. I’ll include what investments we have in that particular account, our stock/bond split as well as our return. I think this is the simplest way to do it without getting too confusing.

- I won’t include our direct real estate investments in this analysis. You can find individual long term annualized return analyses for my properties in posts like this one and more holistic analysis here. This analysis will include only my REIT investments in terms of real estate.

- I won’t include our 529 accounts for our 3 kids as, despite including them in our net worth, they are not “ours.”

- I’m not going to tally this all into net worth as that is not the point of the post. You can see my net worth updates, including the most recent one here.

A quick primer on how I invest

Many of you following will already be familiar with my investing strategy and philosophy. But, for anyone who isn’t, I’ll give just a very quick primer here to put my 2025 portfolio performance in perspective.

I invest in broadly diversified index funds of stocks and bonds in my preferred asset allocation which I rebalance as needed yearly. I initially did this through individual index funds but more recently use the two funds for life approach a la Merriman and Buck.

And I do this because passive investing beats active investing 80% of the time with lower taxes and fees. And rebalancing has been shown to improve returns (albeit slightly). So, any good performance you see here is not attributable to me as a great investor…I simply rode the waves of the overall market tweaking only for my personal risk tolerance via my asset allocation.

You can also see all of this and more in depth in my written financial plan here while, as you may recall, Selenid and I made these 7 changes to our plan on 2023. We had no changes to this plan throughout 2025 and foresee none ahead in 2026.

A quick review of my portfolio performance in 2024

In 2024, our overall asset allocation was:

- 88.7% Stocks

- 9.5% Bonds

- 0.95% Real Estate

- 0.85% Cash/Short Term Reserves

Our goal asset allocation started out at 80% stocks and 20% bonds 3+ years ago. However, as I talk about here, we changed it to 90% stocks and 10% bonds roughly in 2023 and plan to keep it there for the next 5+ years at least.

Meanwhile, our overall return was:

- 14.5%

Ok, with all of that set, let's get into the 2025 portfolio performance…

• I’ve found I can use my medical expertise to earn money in less than 10 minutes.

• During downtime, I knock out quick surveys and get paid for it.

• The money shows up right away in PayPal or gift cards.

• It’s by far the easiest side income I’ve come across and one I actually use.

My 2025 portfolio performance

Again, we will do this based on investment account…

403b

This first category will be broken into my 403b and Selenid’s 403b.

My 403b

This is by far our biggest account. In this account, my investments are split as such:

- 33.63% – TIAA Access Vanguard 500 Index T1

- 11.47% – TIAA Access Vanguard Extended Market Index T1

- 4.28% – TIAA Access Vanguard Small-Cap Value Index T1

- 31.20% – TIAA Access International Equity Index Fund T1

- 4.41% – CREF Inflation-Linked Bond R3

- 12.31% – TIAA Access Vanguard Total Bond Market Index T1

- 3.68% – TIAA Real Estate REIT

The reason I have two small cap funds (Vanguard Extended and Vanguard Small Cap) is because the offerings available in my 403b account surprisingly changed in 2023.

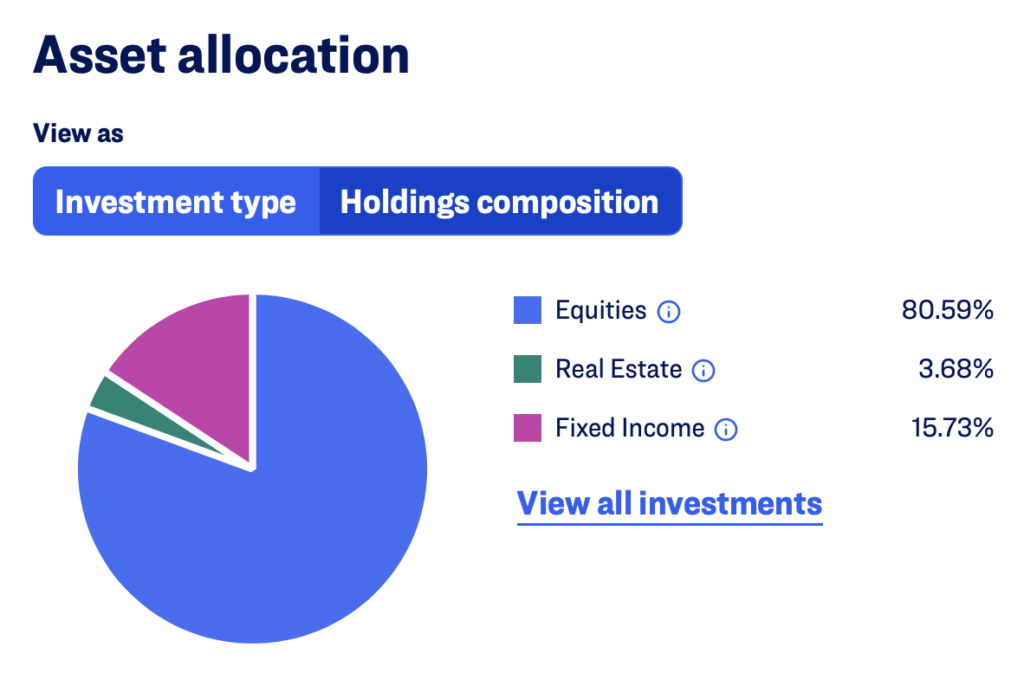

This means that my asset allocation here is approximately:

- 80.59% Stocks

- 15.73% Bonds

- 3.68% Real Estate

And my return over the past year in this account was:

- 18.3%

Selenid’s 403b

In this account, her investments are split as such:

- 46.26% – TIAA Access Vanguard 500 Index T1

- 35.66% – TIAA Access International Equity Index Fund T1

- 7.68% – CREF Inflation-Linked Bond R3

- 7.09% – TIAA Access Vanguard Total Bond Market Index T1

- 3.14% – TIAA Real Estate REIT

This means that her asset allocation is:

- 81.92% Stocks

- 14.77% Bonds

- 3.31% Real Estate

And her return over the past year in this account was:

- 19.9%

457

In 2023, we started to invest the maximum into my 457 account.

In this account, my investments are split as such:

- 90.56% – Vanguard Target Retirement 2060 Fund (VTTSX)

- 9.44% – Vanguard Small Cap Index I (VSCIX)

This means that my asset allocation here is approximately:

- 92.85% Stocks

- 7.15% Bonds

And our return over the past year in this account was:

- 20.58%

Roth IRAs

2023 was the first year as well that Selenid and I both contributed to a backdoor Roth IRA. I invested a bit into a Roth IRA through the “front door” as a resident. And we did it again in 2024.

I’ll break up the analysis therefore between my Roth IRA and Selenid’s Roth IRA.

My Roth IRA

In this account, my investments are split as such:

- 59.15% – Vanguard Target Retirement 2055 Investor Class (VFFVX)

- 26.97% – Vanguard Small Cap Value Index Admiral Class (VSIAX)

- 13.86% – Vanguard Target Retirement 2045 Investor Class (VTIVX)

That means that my asset allocation here is:

- 92% Stocks

- 7% Bonds

- 1% Cash

And my return over the past year in this account was:

- 17.2%

Selenid’s Roth IRA

In this account, her investments are split as such:

- 100.0% – Vanguard Target Retirement 2055 Investor Class (VFFVX)

That means that her asset allocation here is:

- 90% Stocks

- 9% Bonds

- 1% Short term reserves

And her return over the past year in this account was:

- 19.1%

The small difference in returns between our Roth IRA accounts is likely due to the difference in small value tilt among the accounts. This will not happen every year, but it's proof that in 2024, a small value tilt minimally increased returns secondary to the increased associated risks.

Taxable accounts

Our Vanguard taxable account

In this account, our investments are split as such:

- 44.87% – Vanguard Target Retirement 2055 Investor Class (VFFVX)

- 40.43% – Vanguard Target Retirement 2045 Investor Class (VTIVX)

- 14.69% – Vanguard Small Cap Value Index (VSIAX)

This year we made all of our contributions a bit more aggressive by buying shares of the 2055 TDF instead of the 2045 TDF.

That means that my asset allocation here is:

- 89% Stocks

- 10% Bonds

- 1% Cash

And our return over the past year in this account was:

- 19.5%

Our Acorns taxable investment account

I really love Acorns. I don’t have a financial interest but I just think it’s a cool service that basically invests you change. Through it, we’ve invested near $10,000 over the past couple of years.

In any regard, in this account, our investments are split as such:

- 4.88% – iShares Core S&P Small-Cap ETF (IJR)

- 10.09% – iShares Core S&P Mid-Cap ETF (IJH)

- 54.5% – Vanguard S&P 500 ETF (VOO)

- 30.5% – iShares Core MSCI Total International Stock ETF (IXUS)

I choose these based on a “Core Aggressive” portfolio option within the account.

That means that our asset allocation here is:

- 100% Stocks

- 0% Bonds

And our return over the past year in this account was:

- 18.45%

Our E*Trade account

We actually own 1 individual stock. This is housed on an E*Trade account. I received this stock as compensation for consulting work in 2024 and so there's nothing to do but hold it.

That means that our asset allocation here is:

- 100% Stocks

- 0% Bonds

Obviously.

And our return over the past year in this account on this individual stock was:

- -18.0%

My only negative return! Another black eye for active stock picking? Maybe.

This was a free bet that I got to place and so far it has hit overall since I've had it, even if not for 2025. Doesn't mean I believe gambling or speculating is a viable investment strategy though…

• I’ve found I can use my medical expertise to earn money in less than 10 minutes.

• During downtime, I knock out quick surveys and get paid for it.

• The money shows up right away in PayPal or gift cards.

• It’s by far the easiest side income I’ve come across and one I actually use.

Summing it all up

For those keeping track, our overall asset allocation is therefore roughly:

- 89.48% Stocks

- 10.05% Bonds

- 0.47% Real Estate

Our goal asset allocation started out at 80% stocks and 20% bonds 3+ years ago. However, as I talk about here, we changed it to 90% stocks and 10% bonds roughly in 2023 and plan to keep it there for the next 5+ years at least.

So we are right in the ballpark given this transition. No need to rebalance this year! I will point out that this is the second year in a row that we have not needed to rebalance our asset allocation. That is the beauty of having a lot of our investments in target date funds which rebalance automatically.

Meanwhile, our overall return (excluding our individual stock holding) was:

- 19.00%

Obviously, I am really excited and happy about this return. It is even better than our return of 14.5% last year. Does that mean that I am such an incredible investor? Of course not! I just invested passively and the market rewarded me. It could have been a down year and I had bad returns but I would have done the same thing.

Because I’m investing for the long term! Just like you should.

I hope you enjoyed this insider peek into my 2025 portfolio performance. If you are looking to get started or refine your path to financial freedom and are looking for a helpful resource, check out my best-selling book, Money Matters in Medicine or my course, Graduating to Success!

In the meantime, here are some additional useful posts:

- How Much Is Enough Retirement Savings?

- Physician Side Gigs to Make You Passive Money

- The 3 Most Tempting Current Investments to Avoid

What do you think? What was your 2025 portfolio performance? How did you invest? Let me know in the comments below!

2 Responses

You likely have many negative returns among the stocks within your funds.

At your age, dump the bonds!

I do understand that but for me, the asset allocation meets my risk tolerance and I see the bonds serving important role