One of my favorite financial metrics to track each year is expected net worth.

I have written before about both how I calculate my expected net worth as well as my actual net worth and why I use it as a sort of financial report card:

The reason I like this metric so much is simple. It's easy and gives you a compass to see how you are doing financially and what you can be doing better. However, net worth by itself does not tell you much without context.

A net worth of $500,000 might be amazing for one person and disappointing for another. A net worth of $1 million sounds impressive until you realize someone may be approaching retirement. On the other hand, a young physician a few years out of training who reaches a $1 million net worth has likely made tremendous financial progress.

That is why I calculate expected net worth each year and compare it to my actual net worth. It gives me a benchmark. It allows me to compare where I actually am versus where I reasonably should be based on my age, inlincome, and stage of career.

Think of it like getting a report card. The goal is not necessarily to get an A+ every year. The goal is to objectively measure progress.

So, how am I doing?

The Results

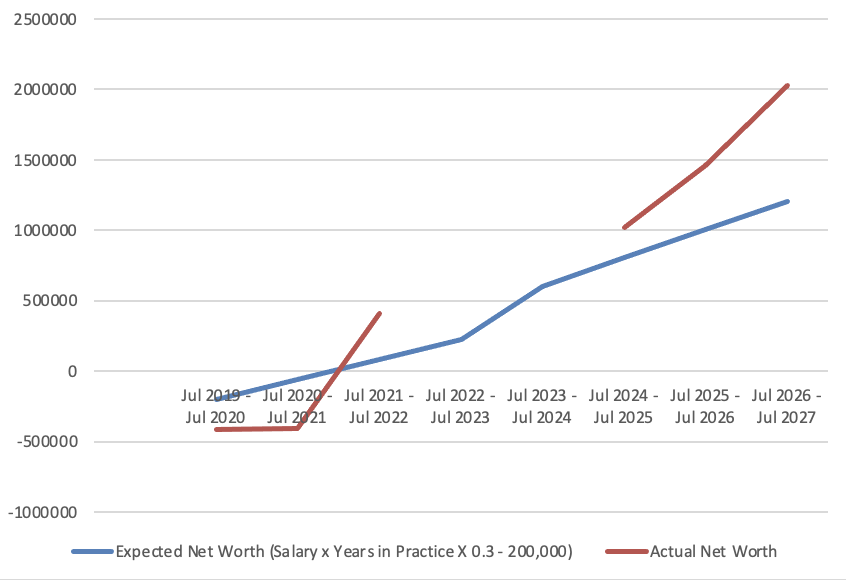

Here are the major checkpoints in my financial journey:

| Period | Expected Net Worth | Actual Net Worth | Difference |

|---|---|---|---|

| Jul 2019-Jul 2020 | -$200,000 | -$412,022 | -$212,022 |

| Jul 2020-Jul 2021 | -$59,000 | -$405,800 | -$346,800 |

| Jul 2021-Jul 2022 | $82,000 | $410,827 | +$328,827 |

| Jul 2024-Jul 2025 | $805,000 | $1,021,905 | +$216,905 |

| Jul 2025-Jul 2026 | $1,006,000 | $1,457,051 | +$451,051 |

| Current Update | $1,207,000 | $2,030,661 | +$823,661 |

Looking at those numbers, one thing immediately jumps out. The gap between expected and actual net worth continues to widen.

Today, my actual net worth exceeds my expected net worth by more than $823,000. That sounds great, but what is more interesting is how we got here.

The Early Years Were Not Pretty

If you had looked at my financial situation during my first couple years as an attending, you probably would not have been impressed. I certainly was not.

After my first year in practice, my expected net worth was around negative $200,000. My actual net worth was negative $412,022. Not exactly a glowing report card.

A year later, things still looked rough. My expected net worth had improved to negative $59,000, but my actual net worth remained below negative $400,000. At that point, I was nearly $350,000 behind the benchmark.

This is exactly why I think expected net worth is such an important metric for physicians. As doctors, we generally spend years accumulating massive student loan debt while delaying earnings through residency and fellowship training. When we finally begin earning attending salaries, we often expect our finances to transform overnight. However lifestyle creep and delayed gratification are powerful forces working against us.

Plus wealth just simply does not work that way.

Those first few years are often spent digging out of a hole. Progress is happening even when the scoreboard does not seem to reflect it. In many ways, those early years are the most important part of the journey because they establish the habits that ultimately determine long-term success.

Then the Flywheel Started Turning

The biggest shift occurred between 2021 and 2022. My expected net worth was just $82,000, while my actual net worth reached more than $410,000.

Suddenly, I was not behind anymore. I was ahead by more than $328,000.

The interesting thing is that there was not one magical event that caused this. There was no lottery ticket, inheritance, or single investment that changed everything overnight. Instead, multiple years of good financial decisions began compounding on one another.

Student debt balances decreased while investment accounts continued growing. Retirement contributions accumulated year after year, and additional income streams started gaining traction. Our real estate investments grew. None of these developments were dramatic individually, but together they created meaningful momentum.

This is one of the most underappreciated aspects of wealth building. For years, progress feels painfully slow. Then, all at once, it feels fast.

The reality is that the growth was happening the entire time. It simply was not visible yet.

The Million Dollar Milestone

One milestone that naturally gets a lot of attention is reaching a seven-figure net worth.

By July 2024-July 2025, my actual net worth exceeded $1 million. My expected net worth at that time was approximately $805,000, so I was ahead by roughly $217,000.

Crossing the million-dollar threshold felt good, but the milestone itself was not the most meaningful part. What mattered was what it represented.

It represented years of consistent behavior. It represented living below my means despite a significant increase in income. And it represented investing when markets were up and when markets were down.

It also represented paying off debt while simultaneously building assets and creating multiple streams of income rather than relying exclusively on my physician salary.

The million-dollar milestone was not created in one year. It was created by hundreds of small financial decisions and habits like these grown over many years.

Why the Gap Keeps Growing

The most interesting part of this exercise is what has happened recently.

The gap between expected and actual net worth is not just staying positive. It is accelerating.

A year ago, I was approximately $451,000 ahead of my expected net worth. Today, that figure is over $823,000, which means the gap has nearly doubled in a relatively short period of time.

In percentage terms, my actual net worth is nearly 70% higher than what the benchmark predicts.

Why?

There are several reasons.

First, investment growth becomes increasingly powerful as your asset base grows. When you have $50,000 invested, a good market year is nice. When you have seven figures invested, a good market year can create wealth at a much faster pace.

Second, my non-clinical income has continued to grow. In fact, in 2025, my non clinical income was nearly $400k! Building businesses, creating additional revenue streams, and diversifying income sources has been a major contributor to my financial growth.

Third, the power of consistency compounds. The financial habits that helped me move from negative $400,000 to zero are the same habits helping me move from $1 million to $2 million. The math simply becomes more powerful.

What This Report Card Really Tells Me

When I first started calculating expected net worth, I viewed it primarily as a score. Now I see it differently.

I see it as feedback.

The number itself is less important than the trend. And the trend tells me a few things.

1. Systems Matter More Than Goals

Goals are helpful, but systems are what actually create results. My financial progress has not come from setting ambitious targets. It has come from consistently following the same processes laid out in our written financial plan year after year.

Those systems include saving automatically, investing regularly, avoiding unnecessary lifestyle inflation, increasing income, and tracking progress consistently.

2. Wealth Building Is Nonlinear

This is perhaps the biggest lesson.

The first few years felt incredibly slow. Today, the numbers move much faster. Many people quit during the slow phase because they assume their efforts are not working. Money contributed to retirement accounts don't seem to grow as fast as we want, especially if the market is down so we sell. We buy one investment property and it doesn't take us to financial freedom so we lose faith in the process.

In reality, we can be too quick to quit right before compounding starts becoming visible. Trust the process, it works. This proves it.

3. Income Matters

I know “just earn more” is not particularly helpful advice. But I do think physicians often underestimate the value of creating opportunities beyond clinical medicine.

Additional income streams have played a huge role in accelerating my financial progress. They have allowed me to invest more, pay down debt faster, and build wealth without relying only on my clinical income.

4. Context Matters

This is the entire reason I use expected net worth. Without context, it would be easy to look at any single number and draw the wrong conclusion.

The benchmark helps me evaluate whether I am actually making progress. It also helps me avoid both unnecessary discouragement and false confidence.

Final Thoughts

When I look at these numbers, I do not primarily see a net worth of $2 million. I see the journey that produced it.

I see a physician who started more than $400,000 in the hole. And I see years where progress felt frustratingly slow. I see consistent investing, debt reduction, and income growth gradually building momentum until the results became impossible to ignore.

Years ago, I was hundreds of thousands of dollars behind my expected net worth benchmark. Today, I am more than $800,000 ahead of it.

The lesson is not that everyone should strive to beat some formula. The lesson is that wealth building works. The formula is right here. There are no secrets.

But it does not work overnight. And it is not without setbacks. And you can't get there without patience (the toughest part for me!).

But if you consistently make good financial decisions and give them enough time to compound, the results can eventually exceed what you ever expected.

What do you think? Do you track your expected and actual net worth? How do they track for you? Was the progress of your wealth building linear or non-linear? Where do things stand now? Let me know in the comments below!