Let me start with something that might sound strange coming from me: Optimism is overrated. At least when it comes to your money. If you look at how most physicians approach their finances, it usually falls into one of two camps. Either there’s this quiet assumption that everything will work out eventually or there’s a low-grade pessimism that makes people avoid engaging with their finances altogether. Neither approach works particularly well. But, together they can actually work quite well. There’s a concept called the Stockdale Paradox that I think explains this perfectly. And, more importantly, gives us a better way forward.

- Tax season may be over, but for physicians with growing income, 1099 work, practice ownership goals, or spouse-side businesses, Q2 is when real tax planning should begin.

- Gelt is a strategy-first CPA firm powered by technology, built for founders, operators, and high-income professionals with more complex financial lives.

- In this live 45-minute webinar, Spencer Carroll, CPA and Rachel Richards, CPA from Gelt will walk through post-April 15 tax planning strategies, including extensions, estimated payments, what physicians can still do now, and how to start planning ahead for 2026.

- New clients this quarter also receive a complimentary 30-minute 2026 tax planning session and a 3-year returns review to help identify missed deductions and missed planning opportunities.

Interestingly, when I think about my past and current financial journey, the Stockdale Paradox has served me pretty well. And understanding it reduced my frustration with the battles between optimism or pessimism that I feel along the way.

The Story (And Why It Matters)

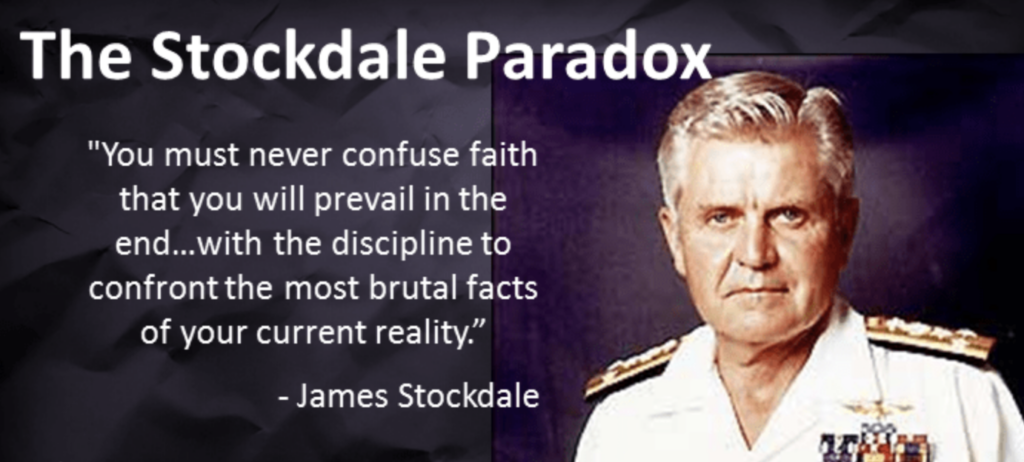

The Stockdale Paradox comes from Admiral James Stockdale, who was a prisoner of war in Vietnam for more than seven years. The story and the “paradox” itself was coined by Jim Collins in his book, Good to Great.

Anyway, when Admiral Stockdale was later asked about those in the prison camp who didn’t make it, his answer caught people off guard. It wasn’t the pessimists who struggled. It was the optimists.

Specifically, it was the ones who kept setting expectations that reality couldn’t meet. They would say things like, “We’ll be out by Christmas.” And then Christmas would come and go. So they’d push it back. “Okay, by Easter.” And then Easter would pass too.

Over time, those repeated disappointments took a toll. They lost faith and sadly lost their lives in the end.

Stockdale’s approach was different. He never lost faith that he would survive and eventually get out. But at the same time, he fully accepted the reality of his situation. How hard it was, how uncertain it was, and how long it might take. And he survived.

That’s the paradox in a nut shell: To be successful, you need unwavering faith in the long term, while fully accepting reality in the short term.

Why Doctors Especially Struggle with This

Medicine wires us for delayed gratification.

We spend your 20s (and often early 30s) grinding through school and training. We put off income, investing, and often basic financial education. All of it is justified by the belief that it will be worth it later.

And to be fair, that belief is often correct as long as the proper steps are taken.

But that often does not happen because there’s a subtle shift that emerges. Our long-term trust in the process can quietly turn into a passive assumption that everything will just simply work out financially.

You start to think:

- “I’ll invest more once things settle down.”

- “My income will make up for it.”

- “I’m a doctor, I’ll be fine.”

The problem is that none of those are strategies. They’re just optimism.

And the result is an arrival fallacy upon finally reaching the end of the road and becoming an attending. And then it either persists in delusion or slowly evolves to cynicism as our career progresses. Both are paths that are much more likely to end in burnout than in financial freedom and career fulfillment.

What Blind Optimism Looks Like in Real Life

I’ve been there myself, and I see it all the time with other physicians.

It doesn’t usually look reckless. It actually feels pretty reasonable in the moment. You’re busy, your income is increasing, and nothing feels like it’s on fire.

But under the surface, things start to drift.

Spending creeps up a little at a time. Investing gets pushed off because there’s always something more urgent. Debt sticks around longer than it needs to because it doesn’t feel like a crisis.

And because your income is high, everything still feels…okay. That’s what makes it dangerous. There’s no forcing function that makes you confront reality until it catches up to you and all of a sudden feels like it is too late (even though it never is).

The Other Extreme (And Why It’s Just as Bad)

On the other side, some physicians swing too far in the opposite direction.

Instead of assuming everything will work out, they start to believe that nothing will. They feel behind, overwhelmed, or frustrated with the system.

That shows up as thoughts like:

- “I’m too far behind to catch up.”

- “The system is stacked against us.”

- “What’s the point?”

So they disengage.

They sit on cash instead of investing. They avoid looking at their numbers. Plus they delay decisions indefinitely. They spend more because it feels like they will never be able to make a positive dent in their finances anyway.

This isn’t realism. It’s resignation. And it leads to the same place as blind optimism, which is stagnation.

The Balance That Actually Works

The physicians who build real wealth aren’t necessarily the highest earners or the most financially savvy at the start. Remember, your income is simply the fuel to your FIRE. If you make $1 million annually but spend $1 million annually, you are not building any wealth. Conversely, you can make $250,000 annually, save 20% of your gross income and invest it wisely and reach financial freedom easily.

What those who are successful do well is hold both sides of the Stockdale Paradox at the same time.

First, they are brutally honest about where they stand. They know their numbers, not approximately, but exactly. They understand their net worth, their spending, and their debt, including interest rates and timelines. There’s no hiding from reality.

At the same time, they maintain a strong sense of long-term confidence. They believe that if they consistently execute a sound plan, they will build wealth. They trust the process, even when results are slow or invisible in the short term.

That combination of clarity plus conviction is what actually works.

As I look back on my story, this starts to seem really familiar. It explains why I felt relief instead of horror when I first calculated my net worth and saw it was -$500k. Yes it was bad, but now I could confront reality while also finally understanding some of the steps I could take to improve my situation, which I never doubted I could improve with the proper financial education and action. Fast forward 6 years and my net worth is over $2 million. It's the Stockdale paradox at work.

Where This Shows Up Most for Doctors

One of the biggest issues for physicians is that high income can mask poor financial habits.

You can earn $300,000 or more per year and still undersave, overspend, or carry inefficient debt. And because your income is high, there’s no immediate pain signal. Everything continues to feel manageable.

Another challenge is the delayed financial start. Most physicians don’t begin earning meaningful income until their 30s, and very few receive formal financial education along the way. That means you’re suddenly making high-stakes financial decisions without much experience.

In that vacuum, optimism often fills the gap.

Then there’s lifestyle inflation. After years of training, it’s natural to upgrade your life. A better house, a nicer car, more convenience. But those upgrades often become fixed expenses, which reduce flexibility and make it harder to change course later.

Applying the Stockdale Paradox to Your Finances

This framework only matters if you actually apply it.

The first step is to get clear on your numbers. That means calculating your net worth, understanding your monthly spending, listing out your debts with their interest rates, and determining your savings rate. Not estimates but real numbers.

Once you have that, the next step is to accept what you see. You may not like it. In fact, you probably won’t. But that’s the point. You can’t improve a situation you haven’t clearly defined.

From there, it’s important to reset your expectations. Financial progress, especially for physicians starting later, is not a quick process. This is a long game measured in years and decades, not months.

Finally, you build systems that reduce reliance on motivation. Automatic investing, consistent savings plans, and a defined spending framework allow you to make progress without constant decision-making.

A Simple Example

Let’s say you’re 35 years old with $250,000 in student loans, $50,000 saved, and an income of $300,000. Blind optimism would look at that situation and say, “I’ll be fine.” Brutal reality would point out that your net worth is still negative and that your current habits matter more than your income.

The Stockdale approach combines both perspectives. It acknowledges exactly where you are today, without sugarcoating it. But it also recognizes that with consistent execution over the next 10 to 15 years, you are very likely to build significant wealth.

There’s no panic in that mindset, but there’s also no denial.

What This Looks Like in Real Life

In practice, this mindset shows up in small but important ways.

When the market drops, you don’t panic because you expect volatility. You continue investing because your long-term belief hasn’t changed.

When paying off debt feels slow, you don’t abandon the plan. You accept the pace and keep moving forward.

When progress feels invisible in the early years, you don’t assume something is broken. You understand that compounding takes time.

The Bottom Line

Most physicians don’t struggle financially because of a lack of income. We struggle because they either avoid confronting reality or they lose belief when reality isn’t ideal.

The Stockdale Paradox solves both problems. It forces you to look clearly at where you are, while maintaining confidence in where you’re going.

Face reality. Keep the faith. Repeat. That’s the entire framework.

Take Action

If you take one thing from this, make it practical.

Set aside 30 minutes this week and figure out your real financial numbers. Not what you think they are, but what they actually are.

Because until you do that, you’re not managing your finances. You’re just hoping.

Here are some resources to help no matter what stage you are at right now:

- 5 Ways For Doctors To Optimize Their Retirement Planning

- Why I Don’t Panic When the Market “Drops”

- 12 Steps to Financial Freedom That Made Me a Better Physician

- The First 7 Steps I Recommend When Doctors Feel Stuck

What do you think? Where do you fall on the optimism-pessimism spectrum when it comes to your finances? Are doctors particularly susceptible to this? Could the Stockdale paradox help? Let me know in the comments below!

2 Responses

Many Drs suffer from Financial Decision Paralysis.

Not making a decision is almost as bad as making a wrong decision.

Invest early and often. Live below your income but don’t scrimp. Reinvest dividends . It’s really not that hard.