What is the definition of financial freedom? The simplest one is that it means you have enough money either saved up and invested or coming in via passive means that you can use to cover all of your living expenses without having to work for the rest of your life. You can then live your life independent of financial considerations. While no predictive tool is perfect, the Rich, Broke, or Dead calculator is pretty darn good.

Markets feel uncertain. Inflation, rates, recession concerns, and stock valuations have many physicians asking where to put capital next.

- Join Carlton Lane Capital on Wednesday, May 20 at 8:00 PM ET for a live webinar on real assets that may hold up when markets do not.

- The session will cover recession-resistant asset classes including housing, industrial real estate, infrastructure, energy, medical real estate, and necessity-based assets.

- Carlton Lane Capital works with accredited investors seeking curated private real estate opportunities, with a focus on diligence, risk visibility, structure, and long-term alignment.

- If you are looking beyond Wall Street for tax-aware, hard-asset investing strategies, this webinar is worth attending.

And the other day, I had a lot of fun running different scenarios on the calculator to get an even more granular sense of my current financial situation as well as any and all prospective future ones.

As always, I am an open book. So let's take a look at all of the simulations I ran and what it means for me. The ultimate goal is to encourage all of you to take a similar look. And remember, where you are now is not where you will be in the future. If you don't like what you see, get started building the basic financial habits that will get you where you want to be in the future.

The Rich, Broke, or Dead calculator explained

The calculator comes from a site called EngagingData. To be honest, I'm not even sure who is behind it and it seems like he or she likes it that way for the most part.

In any event, the calculator is extremely robust. Maybe even a little too complicated for what it needs to be (remember I live my life according to the organizing principle of K.I.S.S.). Either way, it is clear that the designer has a strong background in computer science and a keen interest in finance.

The creator describes the calculator as an “interactive post-retirement fire calculator and visualization looks at the question of whether your retirement savings can last long enough to support your retirement spending and combines it with average US life expectancy values to get a fuller picture of the likelihood of running out of money before you die.”

Basically, you put in a bunch of variables regarding your personal financial situation and it spits out a chart providing the percentage likelihood that, at a certain age, you will be rich (i.e. have enough money to cover expenses), broke (i.e. will not have enough money to cover expenses), or dead (i.e. not alive).

The goal is to have your money at least last as long as you do within a reasonable probability.

Ok, enough background, let's look at some of my simulations!

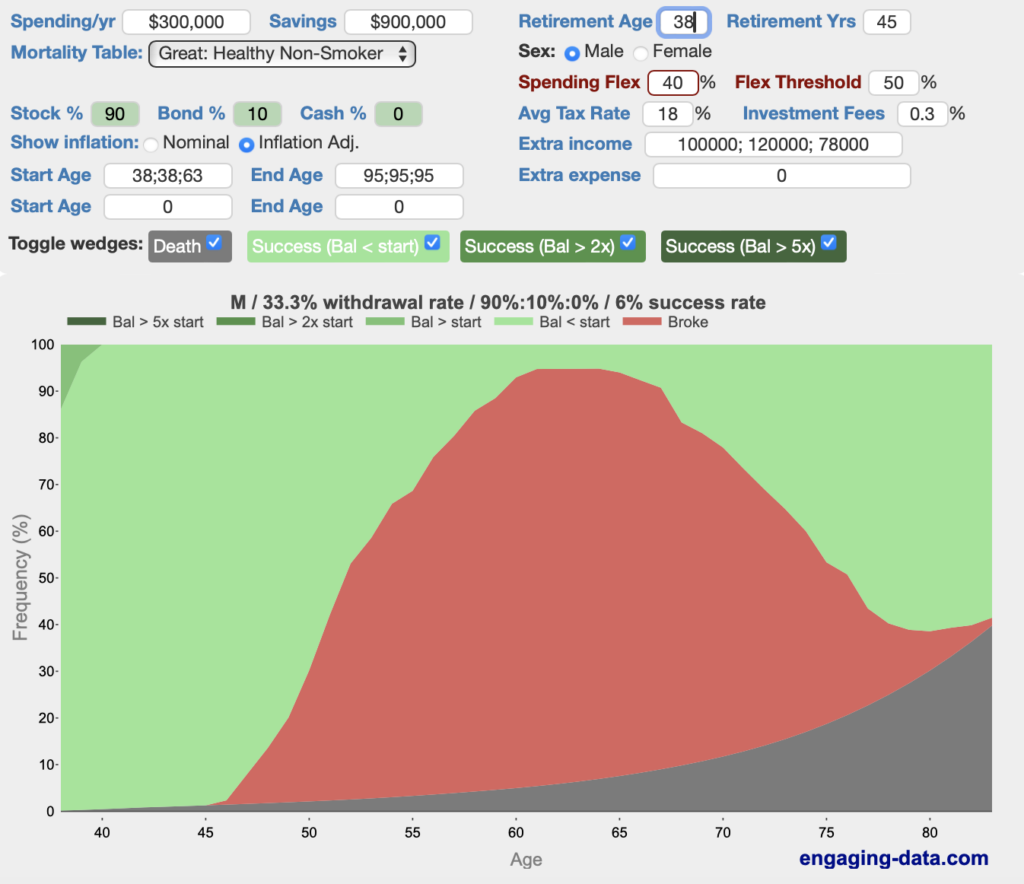

Simulation #1: I retire right this moment

In this scenario, I walk out of the doctors' lounge I am in right now and never come back. My data comes directly from my most recent net worth calculations.

Not great. Overall, I have a good chance of my money not lasting at least as long as I do once I reach age 45.

But let me point out a few things:

- This simulation assumes that I will keep the same level of spending that we currently have which includes: private school for 3 kids, our primary home mortgage, a mortgage on our STR which is not cash flowing yet, and a car payment.

- I did add in a bit of a spending flex. Meaning that if our portfolio fell below 50%, we would cut expenses by 40% by eliminating things like private school and our second mortgage. We could of course go further in eliminating expenses by moving to another house etc. But that is not what we want.

- I include my side income which is becoming more and more passive and includes real estate and my blog. I also include expected social security income.

- My estimated tax rate is based on my recent years' effective tax rates and expected lower income in these years

Obviously, this is not ideal. So let's look at another simulation.

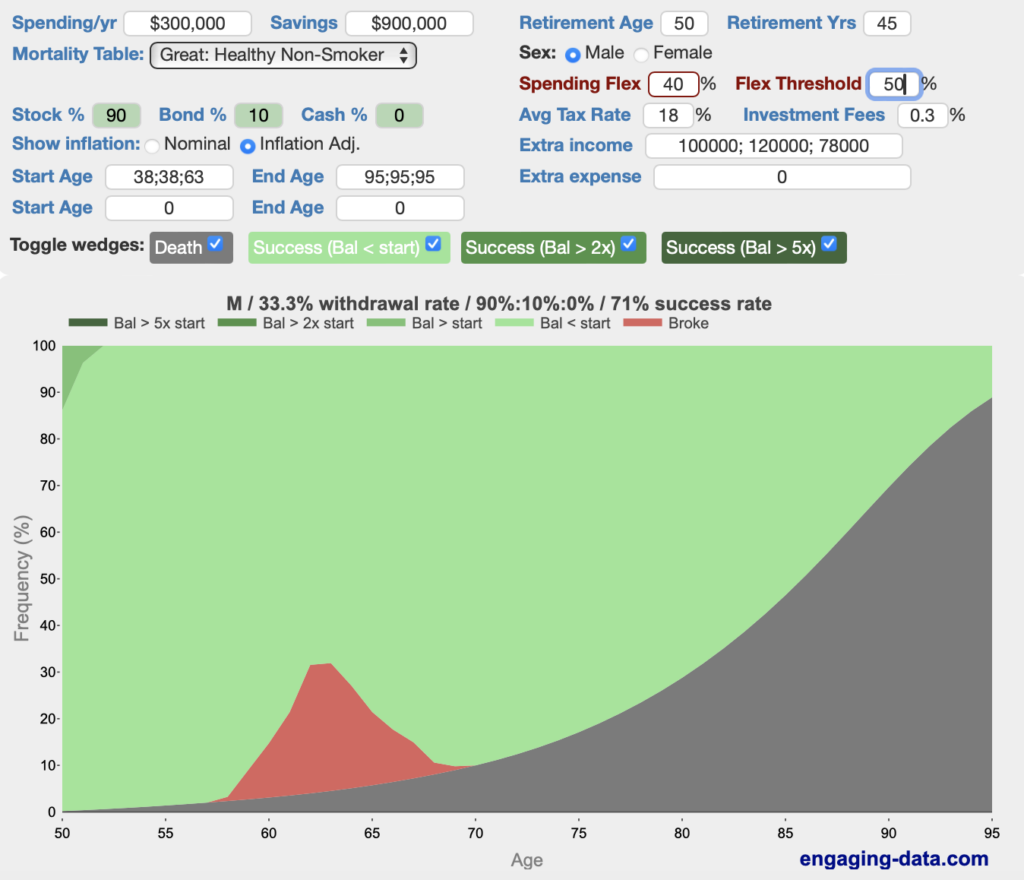

Simulation #2: I don't save another dime, but retire at age 50

Here, I am simulating a situation where we do not contribute another $1 to either our retirement accounts or towards new passive income. However, instead of retiring right now, I retire at age 50. In fact, I am over conservative here saying that my current retirement investments would not grow between now (age 38) and age 50.

Overall, pretty smooth sailing here. A great chance that my money lasts as long as I do. There is a small blip between ages 58 to 68 where there is a peak ~30% chance of running out of money. But otherwise, this looks promising.

Note again that our spending did not change and I kept a spending flex in there.

On to another simulation…

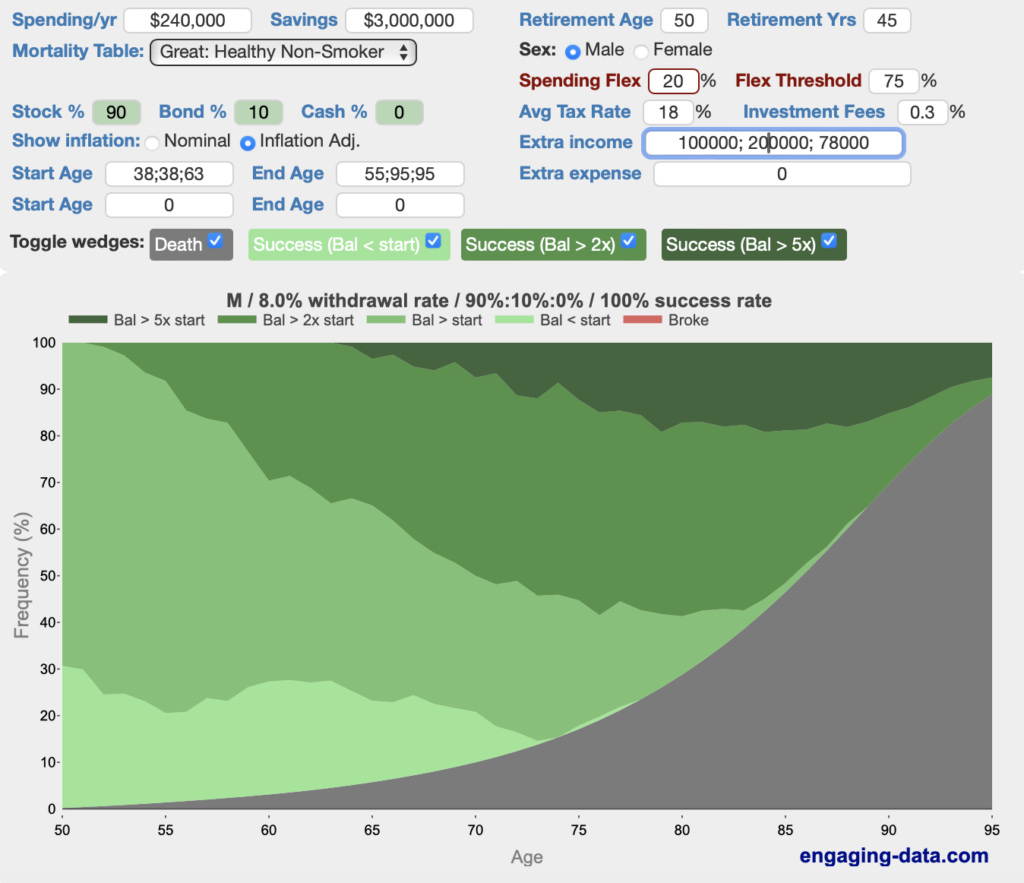

Simulation #3: My ideal retirement scenario

Let's take a peek…

This simulation takes into account all of my retirement goals as listed in my written financial plan with some conservative adjustments:

- Higher estimated spending of $20k monthly

- My passive income from the blog stops at 55 (I have no plans to end this at any time right now)

- I retire at age 50 (12 years from right now)

- I continue contributing to retirement accounts at a similar pace which will get me to an estimated $3M in 12 years based on a conservative return of 5% annually

- Our passive income from real estate increases to $200k (still below the stated goal of $250k annually in our financial plan)

Even with this conservative estimate, our money lasts longer than we do with as close to 100% probability that this algorithm can reach. In fact, the most likely scenario is that we die with more money than we started with, leaving some to our kids.

What does this all mean to me?

Honestly, there were not many surprises here for me.

In simulation #1, I knew that I had not yet reached financial freedom if my expenses weren't adjusted dramatically. That isn't something that Selenid or I want to do right now. We could if we had to. But I still really love what I do and enjoy it. So there is no immediate plan to retire.

For simulation #2, it is interesting to see that we could contribute basically nothing more towards retirement and still retire at age 50 and likely be just fine. This is a good lesson for me as I still have a very hard time spending money right now. I can draw back on these estimates to show that I have a good amount of flexibility no matter what it feels like based on how I grew up with money.

And for simulation #3, it shows that our written financial plan makes sense. This is something we spent a lot of time intentionally thinking through. These numbers just support our initial assumptions even more.

What should it mean to you?

Honestly, not much in terms of absolute values. My situation is different from yours which is different than everyone else's. Personal finance is just that…personal. Everyone has different goals and there are no right or wrong answers.

However, the exercise itself is very valuable. That is what I hope to demonstrate. I encourage you to run the Rich, Broke, or Dead calculator for your own situation and create various simulations. You might like what you see. Or you might not. Either way it is extremely valuable.

If you like what you see, use it as motivation to keep doing what you are doing. See if there are any little tweaks to optimize things even more. But don't obsess.

If you don't like what you see, give yourself some grace. Today is not the finish line. And while the best day to start was yesterday, today is next best. See what little steps you can take to build long term habits to reach your goals.

These resources of mine can help you get started on or optimize your path to financial freedom:

- The 7 Step Basic Formula for Wealth as a Physician

- 5 Important Wealth Building Strategies for Late Career Doctors

- The 1/3 Rule That Helped Me Build Wealth Fast

- 7 Financial Habits of Highly Successful Physicians

What do you think? How would you run a retirement analysis with the Rich, Broke, or Dead calculator? If so, what did you find? If not, what do you think it would show? Let me know in the comments below!