One of the most important concepts in investing is also one of the hardest to follow: to be successful, you need to invest in the overall market for the long term. On the surface, this sounds simple. In practice, it is anything but. As physicians, we are wired to act. We diagnose, intervene, and improve outcomes through action. That mindset serves us incredibly well in medicine. But in investing, it can work against us.

The biggest threat to long term investing success is not a lack of intelligence or effort. It is our own behavior.

Why Smart Doctors Try to Outsmart the Market

There are two common traps that physicians fall into when investing.

First, we assume we have an informational edge. We are used to being high performers in complex environments. It is natural to think that we can identify trends or opportunities that others cannot. This leads to attempts to “beat the market” or generate alpha. When you combine this with investments in the healthcare space, familiarity bias can really derail physician investors.

The problem is that financial markets are highly efficient. Any perceived advantage is quickly erased. Even professional fund managers with vast resources struggle to consistently outperform the market. For individual investors, the odds are even lower.

Second, we equate activity with improvement.

In medicine, doing something often leads to a better outcome. In investing, doing more often leads to worse results. Frequent buying, selling, and adjusting can introduce mistakes, increase costs, and ultimately reduce returns.

The paradox is this: the less you do, the better you tend to perform.

A Simple Visual That Changes Everything

To understand why long-term investing works, it helps to look at the market from different time frames.

Let’s use the S&P 500 as an example. If you zoom in very close on the day I am writing this post, the picture looks discouraging:

- Over one day: down about 1.5%

- Over one week: down about 2.8%

- Over one month: down just over 5%

- Over three months: down around 5.5%

- Over six months: down about 2.8%

If this is the lens you are using, the market looks unstable and unpredictable. It is easy to feel anxious. It is easy to want to pull your money out.

Now zoom out.

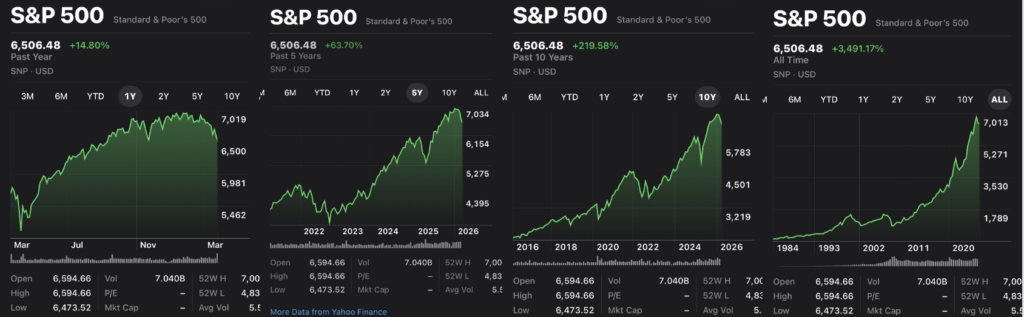

- Over one year: up about 14.8%

- Over two years: up about 24%

- Over five years: up about 63%

- Over ten years: up over 200%

- Over the long term: up roughly 3,500%

Same market. Completely different story.

This is the visual that every investor needs to internalize. Short-term volatility is noise. Long-term growth is the signal.

Why the News Cycle Works Against You

If long term investing is so effective, why is it so hard to stick with? Because everything around us is focused on the short term.

Financial news highlights daily fluctuations. Headlines amplify fear. Global events create uncertainty. Whether it is geopolitical conflict, rising oil prices, or economic concerns, there is always something that makes the outlook seem bleak. When you focus on recent events, it is easy to project that negativity into the future. Even though we know we cannot predict the market and we are smart people, we still try.

This is where many investors make their biggest mistake: they react. They sell when the market drops. They wait for things to “feel safer.” Then they buy back in once prices have already risen.

That cycle consistently destroys value.

The Cost of Getting Out at the Wrong Time

Selling during a downturn feels logical. In reality, it creates two major problems:

First, you miss the opportunity to buy when prices are low. Market declines are effectively stocks going on sale. If you are not investing during those periods, you are missing one of the biggest drivers of long-term returns.

Second, you cannot reliably predict when the market will recover.

Trying to “time the market” is often described as trying to catch a falling knife. No one consistently knows when the bottom has been reached or when the upward trend will resume.

As a result, many investors sell at low prices and buy back at higher prices. That is a guaranteed way to underperform.

How to Stay Invested When It Feels Uncomfortable

Understanding the importance of long term investing is one thing. Sticking with it is another. The key is to build a portfolio that aligns with your risk tolerance.

Stocks offer higher potential for growth but come with more volatility. Bonds are more stable and help preserve value but typically offer lower returns. By including an appropriate allocation of bonds, you can reduce the overall volatility of your portfolio. This makes it easier to stay invested during market downturns.

If your portfolio is too aggressive, you are more likely to panic and sell during a decline. If it is appropriately balanced, you are more likely to stay the course.

The goal is not to eliminate risk. It is to manage it in a way that allows you to remain consistent.

Adjusting Your Strategy Over Time

Your investment approach should evolve as your career progresses.

Early and mid-career physicians have time on their side. The priority during this phase is growth. A higher allocation to stocks makes sense, and short-term volatility is less concerning because you have years or decades before you need to access the funds.

As you approach retirement, the focus shifts. Within five to ten years of needing your money in retirement, preservation becomes more important than growth. This often means increasing your allocation to bonds or other stable assets. Some may also consider additional tools such as single premium immediate annuities, depending on their goals.

The key is that your strategy should match your timeline.

The Wide Lens Matters Most

The most important takeaway is simple: zoom out. You are not investing for today, this month, or even this year. You are investing for the next 10, 20, or 30 years.

There will be down days. There will be down months. Heck, there will even be down years. None of that changes the long-term trajectory of a broadly diversified market.

As physicians, we are trained to focus intensely on the immediate problem in front of us. In investing, that instinct can lead us astray. The investors who succeed are not the ones who react the fastest or analyze the most headlines. They are the ones who maintain perspective.

They ignore the noise. And they stay consistent. They trust the process. And most importantly, they keep their eyes on the long term.

What do you think? What time frame do you invest for? How do short term fluctuations affect you? Do you feel your risk tolerance is well reflected in your portfolio? Let me know in the comments below!